Rapid Manufacturing Was Supposed To Be A Great Business…

Upload a CAD file.

Get an instant quote.

Route the work to a supplier.

Take a cut.

Repeat forever.

On paper, rapid manufacturing looked like one of those beautiful internet businesses that should have worked absurdly well. It solved a real pain point. It had software in the loop. It touched a massive industrial market. And it sat right in the middle of one of the oldest, clunkiest workflows in engineering: emailing drawings around and waiting for shops to get back to you.

And to be fair, these companies were not wrong about the problem. The problem was and is very real. Engineers do want instant quotes. Procurement teams do want a cleaner workflow. Startups do want prototypes and low-volume parts fast. The software mattered. The automation mattered. The marketplace layer mattered. The issue is that making manufacturing easier is not the same thing as making manufacturing a great business. That is where the whole sector started to wobble.

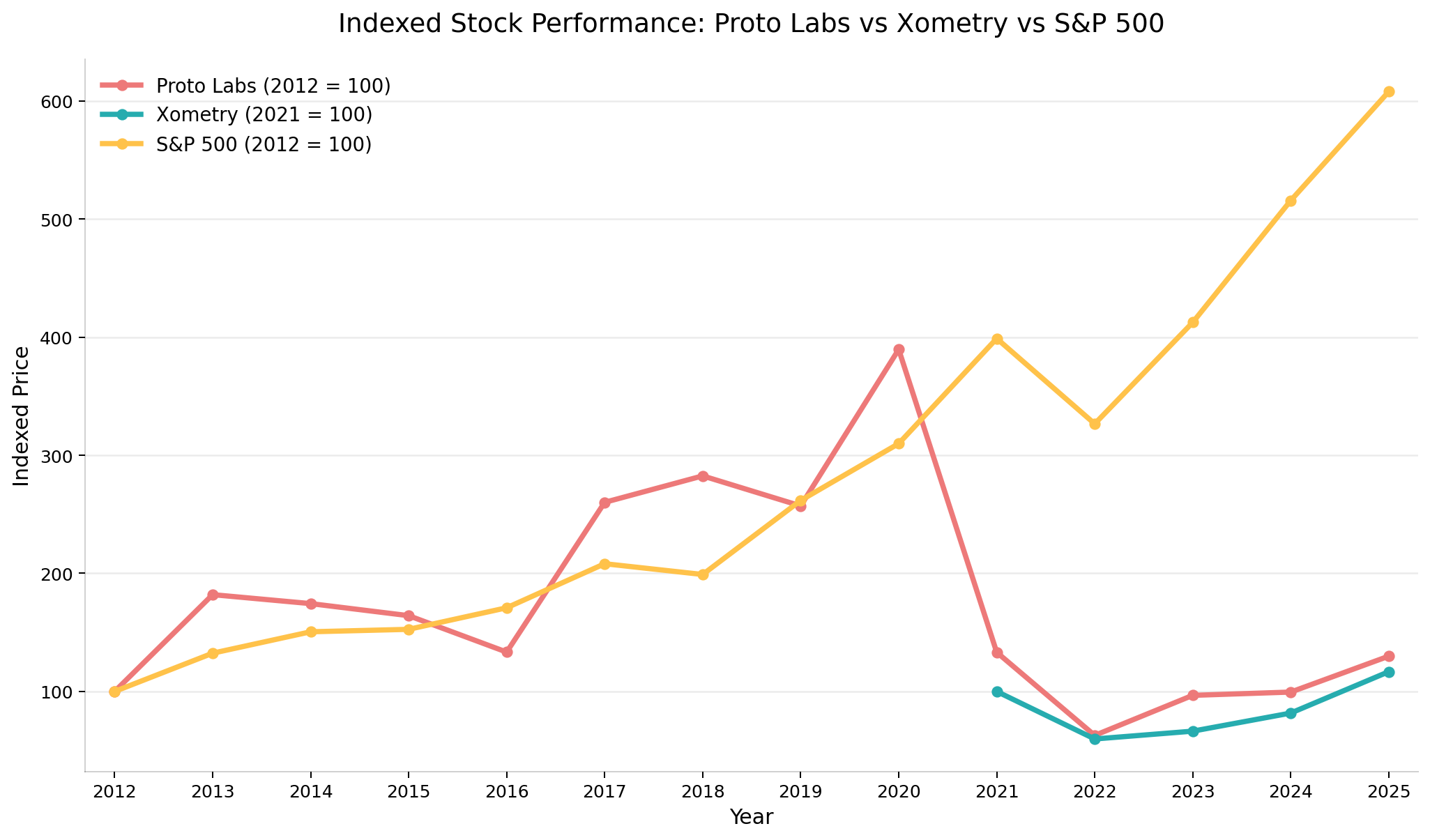

The cleanest way to understand the history of the space is through three companies: ProtoLabs, Xometry, and Fictiv. Each one represents a slightly different attempt to modernize custom manufacturing. Each one did something genuinely impressive. And each one, in its own way, ran into the same ugly truth: rapid manufacturing is operationally heavy, margin-constrained, and much harder to scale profitably than it might initially appear.

Protolabs: The Company That Proved The Category Was Real

If there is a founding success story here, it is Protolabs.

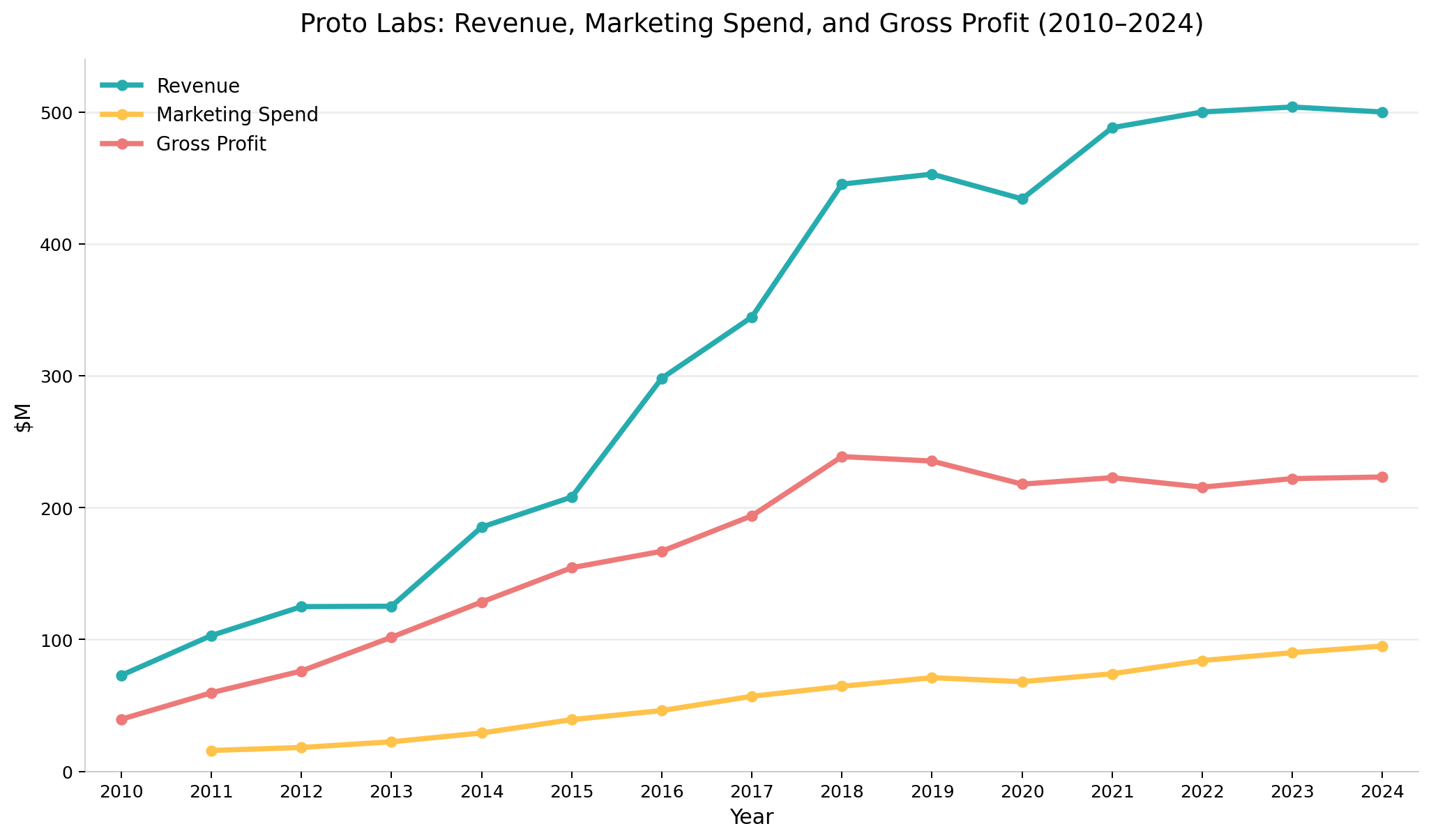

Protolabs was founded in 1999 and built a real, durable business around digitally enabled custom manufacturing. It did not start with some giant “marketplace for everything” vision. It started with a narrower and more controllable model: use software and automation to quote and manufacture prototype and low-volume parts quickly. Over time it added more processes, more geographies, and eventually a broader outsourced network. That is important. Protolabs proved this category was not fiction. Engineers really would upload files, buy custom parts online, and come back if the experience was good enough.

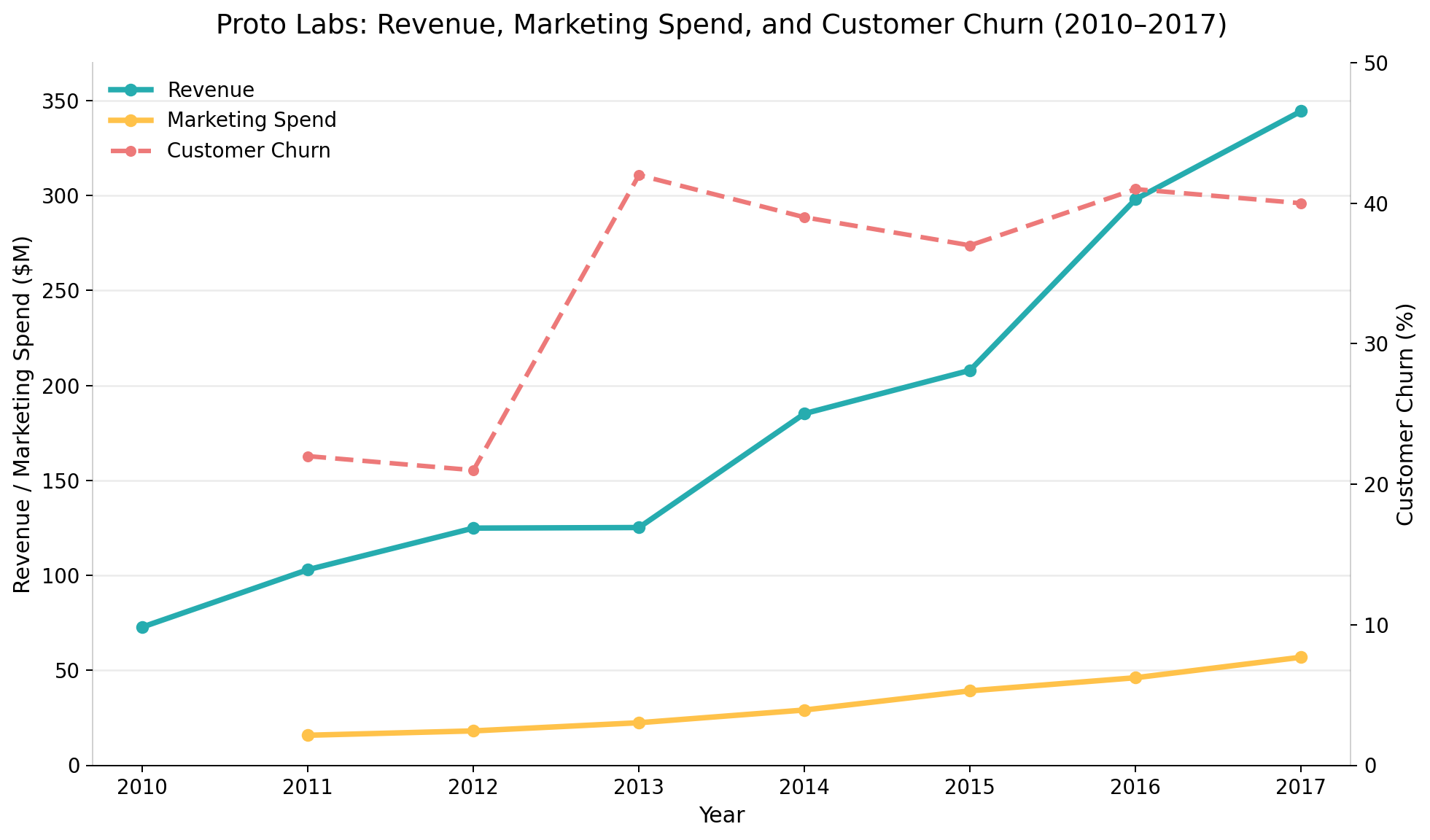

The good news for Protolabs was that the model worked well enough to become a real public company. The less-good news was that the limits of the model also became visible over time. Early on, Protolabs explicitly disclosed both new and existing customers. No one does this anymore as it highlights the biggest issue in the industry, CHURN. They stopped reporting this in 2017 and the rest of this analysis assumes that 40% churn continued, and that the other players experienced similar numbers. Note that this is a big assumption which may not hold, but it is without question that you can see the churn flatline from 2013-2017 between 35% and 45%, and we have no significant reason to believe that the underlying problems inherent in the industry were addressed for them or anyone else based on CAC/revenue/profit over time.

That makes sense if you think about how engineers actually use rapid manufacturing. A team prototypes a part, tests it, revises it, orders again, and then either kills the project or moves it to a different supplier for production. Great for near-term revenue. Not necessarily great for beautiful long-term customer economics. Protolabs could still make money because its model had more control and better margins than a pure marketplace, but even there the cracks showed. From 2016 to 2024 the revenue per customer stabilized right at $9,000 and GP/customer shrank from $5,300 to $4,300. Given the Customer Acquisition Cost (CAC) was $4,000, the payback period for a customer was a full year and the marketing spend was already going into the churn problem so gross profit flatlined from 2018-2024.

There is also a more practical complaint you hear from engineers all the time with Protolabs: parts get there fast, but tolerances and pricing aren’t always competitive. That is not really a surprise. If you build your whole brand around speed and convenience, somebody is paying for that speed. Usually the customer.

Protolabs ended up being both the strongest proof that digital manufacturing is real and one of the strongest proofs that this is not SaaS. The company built a strong, useful, defensible service, but not the high margin software one they were hoping to.

Xometry: Bigger Vision, Harder Economics

Protolabs proved the category was real, but Xometry tried to build it bigger.

The vision was more ambitious from the start. Instead of relying on owned manufacturing capacity, Xometry positioned itself as an AI-enabled digital marketplace connecting buyers and sellers across a fragmented manufacturing ecosystem. In its own words, buyers upload CAD files, Xometry prices them using its instant quoting engine, and the platform routes work to “vetted” suppliers while growing buyer and supplier activity on both sides. It is a very compelling pitch because it promises a business that gets stronger with scale: more buyers attract more suppliers, more suppliers improve pricing and availability, and the resulting flywheel pulls in more buyers.

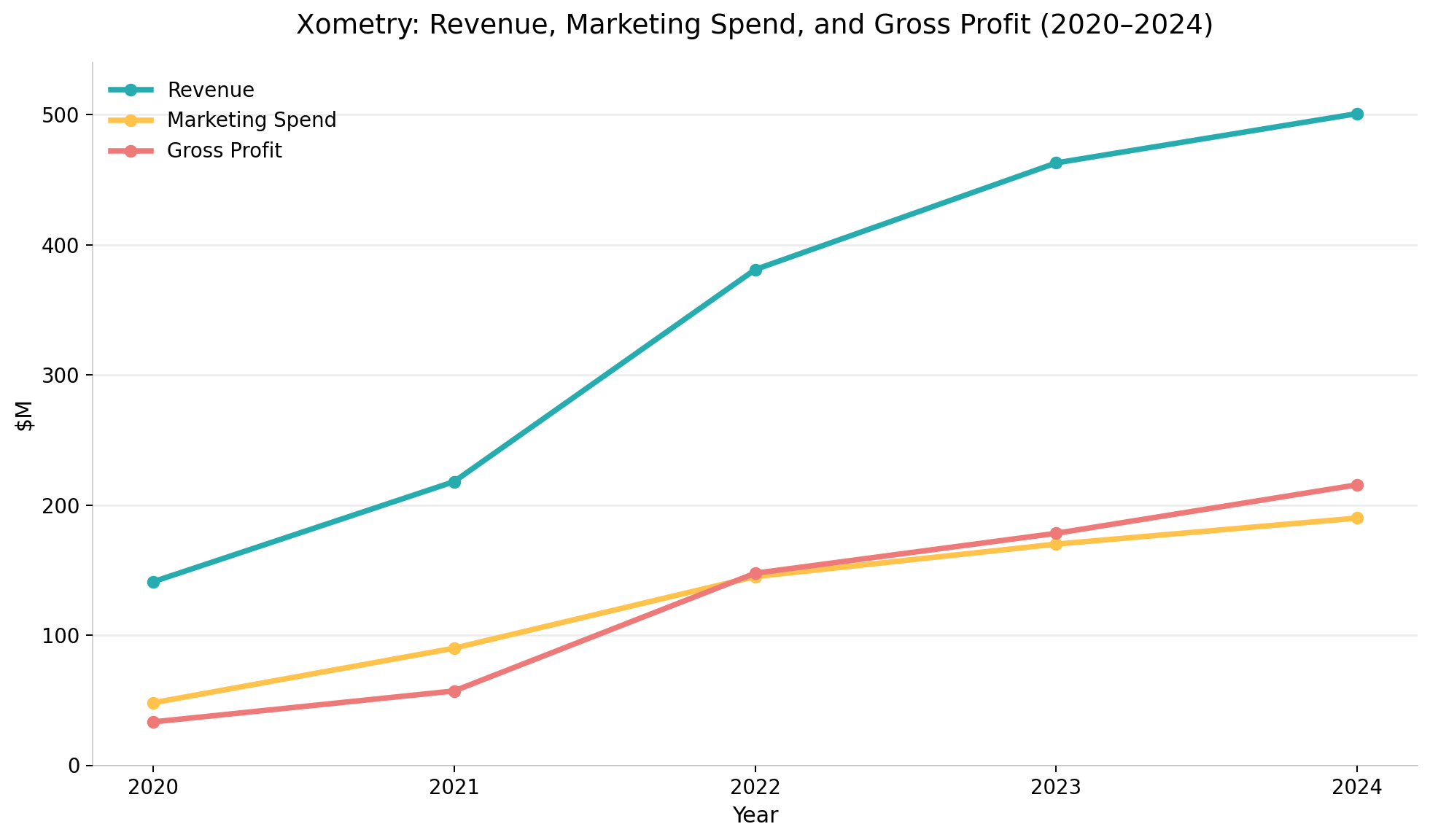

And Xometry really did scale. By the end of 2024, it had 68,267 active buyers, up from 55,325 in 2023, and 4,375 active suppliers, up from 3,429. Those are not vanity numbers. That is a serious platform. It also kept widening the offering with supplier services, marketing services, financial products, and software. On the surface, this looks exactly like what you would want from a digital industrial platform.

But the filings are also unusually honest about how expensive that growth is. Xometry says outright that it will “continue investing in AI, machine learning, cloud infrastructure, international expansion, supplier development, and sales and marketing, and that those investments occur before benefits are recognized", if they are recognized at all.”

Xometry hasn’t seen the Protolabs plateau yet, but it’s likely on the way. When your revenue per customer is $7-9k/year and CAC is $5-6k with 28% gross margins there is a payback period per customer of ~2.5 Years.

There is also a product problem buried inside the model itself. One of the biggest complaints engineers have with Xometry is the black-box nature of the quoting and sourcing flow. You upload a part, get a number, and in many cases have no idea who is actually making it. On two different orders, the answer might be two completely different suppliers with two totally different capabilities, surface finish standards, communication styles, and tolerance discipline. That is great for marketplace flexibility. It is less great if you are trying to build confidence that the fifth order will look and feel like the fourth one. The platform abstracts away the supplier, which is part of the convenience, but it does so in a way that makes repeatability feel shakier than customers want.

Fictiv: Strategic Logic, Tough Math

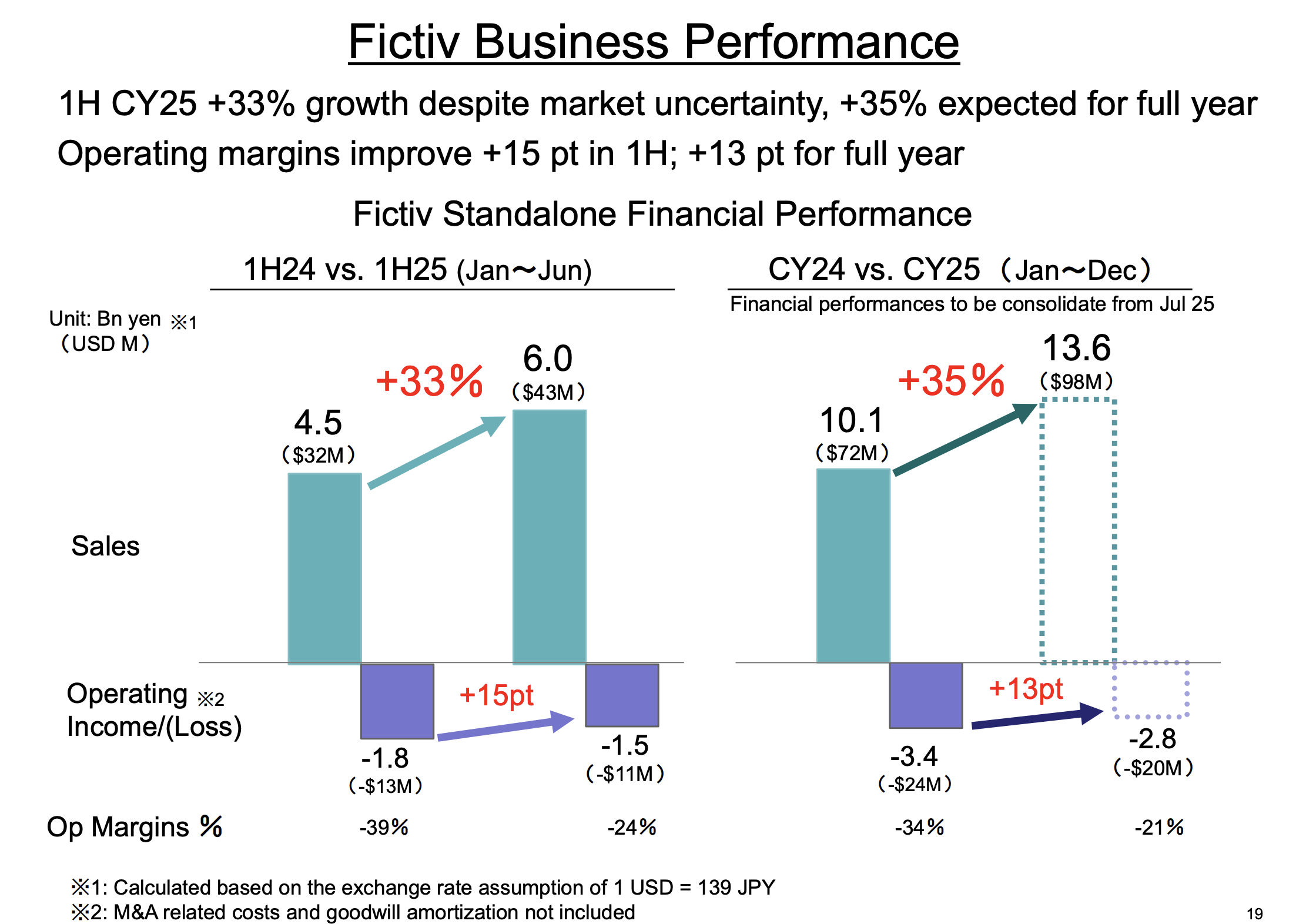

Fictiv is probably the clearest example of how difficult the model can get. It raised about $188M, was reportedly valued around $1B+ at the peak, and sold to MISUMI in 2025 for $330M. Once MISUMI started consolidating Fictiv in July 2025, the FA segment (where Fictiv was added to within Misumi) immediately showed the pattern you would expect from a low-margin acquired marketplace business: sales up, profit down.

Misumi released their Financial 2025 year in review document here where they have specific breakouts for Fictiv business performance as shown in the graphic below. $98M in revenue, -$20M in operating income.

Though their operating margins improved as a result of the consolidation, -21% operating margins still leaves something to be desired. If you factor in the $27M spent on “M&A associated costs” and goodwill amortization (usually a sign that the reported acquisition optics are rough), Fictiv lost Misumi almost $50M in Y1 post acquisition.

To quote Misumi:

”As with sales, Pre-Fictiv consolidated profitability increased due to improvements from the initial plan. Post-consolidated profits declined due to impact of Fictiv acquisition.”

Protolabs’ sale is especially impressive given -34% operating margins the year prior. Based on these numbers, my presumption is that Fictiv follows a very similar trend to Xometry and Protolabs: high CAC (customer acquisition cost), high churn, so their best way to juice revenue was to increase marketing spend to acquire customers faster than they churn.

I am curious to see if the synergy plan Misumi has developed of accelerating Fictiv growth by leveraging Misumi factories and manufacturing partners while cross selling to existing Misumi customers pans out. The trendline is good given the substantial improvements in operating margin already since joining Misumi, and Misumi is “aiming to achieve Fictiv standalone profitability, no later than FY27.”

Why Jiga Might Actually Fix Rapid Manufacturing

The history of this space makes one thing pretty clear: the problem was never demand. Engineers absolutely want faster quoting, clearer communication, and a better way to buy custom parts. The problem was that too many companies tried to force manufacturing into a pure software pattern. They optimized for speed at the top of the funnel, but left too much ambiguity, too much supplier opacity, and too much operational mess underneath. Jiga’s approach looks different. Jiga explicitly does not do instant quotes, instead offering human-reviewed quotes in 24 hours and direct communication with vetted manufacturers. In other words, it is built around the reality that good manufacturing is still a relationship business, and the software should support that rather than pretend to replace it.

That matters because the ugliest economics in this category usually come from the same handful of problems: quoting mistakes, bad handoffs, poor supplier fit, expensive exceptions, and customers who churn once the job gets more complex. Jiga seems designed to attack those exact weak points. Its pitch is not “throw a CAD file into a black box and hope for the best.” It is closer to: keep the manufacturer in the loop, keep the communication visible, use AI to remove the administrative sludge, and make sourcing feel like an extension of the engineering team instead of a totally separate function. The company describes itself as handling quoting and communication in one place, using AI workflows for the repetitive admin work, and giving visibility from prototype through production. That is a much more believable way to improve margins and retention than just chasing more RFQs with more automation.

On the downside, Jiga’s supplier network is still considerably smaller than the established players, a natural constraint for a younger company that vets manufacturers more selectively. On the bright side, the suppliers listed do seem to have a broad repertoire of possible manufacturing processes and work they are capable of, and are very geographically diverse (though strong emphasis is on USA and Chinese vendors). ITAR/ISO work is possible when needed.

Story time: When I was co-oping at Relativity back in 2020, I was one of 4 interns. I was on the propulsion team which exclusively hired PhDs at that point, so they pretty much thought I would be useless for anything more than grunt work until I proved them wrong. As such, the first task they gave me was to source ~30 different parts for the rocket gimbal subassembly, some COTS, some custom (DMLS, heat treat, wire EDM, CNC). Not as illustrious as I thought it would be, but boy did I tackle it with gusto (once convinced a bolt supplier to sell me bolts below cost by pitting them against a rival supplier), and I can say with absolute certainty it would have been way simpler if Jiga existed at the time. Instead, what I did was reach out to about 50 suppliers with emails and calls and dozens of back and forths in order to obtain a few quotes. Something you don’t learn until it happens, is that when a supplier later makes a mistake, it’s the good ones that tell you, but either way you basically have to work with it unless you want to purchase more raw material, have an abundance of timeline (literally never happened), and kickoff the project with a whole new vendor from scratch. The easiest way to tell quality was actually to visit each vendor in person to see how the sausage is made. Luckily I just wanted to be helpful and didn’t mind visiting every shop in a 50 mile radius for the learnings alone, but I definitely wish Jiga had been around at that time for me to use; having easy access to vetted suppliers would’ve let me handle way more of the fun stuff sooner by preventing me from getting bogged down in the sourcing swamp.

Unlike Protolabs and Xometry, Jiga is not a public company, so they do not disclose full financials, but the company does report an annual activated customer churn rate under 11%, an extremely stark contrast to the ~40% churn rates seen historically across the category. Additionally, in late 2025 they announced a $12M Series A led by Aleph, with participation from Symbol and Y Combinator, and on its own materials the company says it is cashflow positive and growing fast. That does not guarantee success, but it is a very different starting point from the “prioritize growth ahead of profitability” playbook that has burned so many others in this category. If Jiga can keep doing what it appears to be doing — using software to cut friction, using people where judgment still matters, and helping teams scale from prototype into production without losing clarity — it has a real shot at solving the exact problems that made the first generation of rapid manufacturing platforms so hard to love.

Note: Though this article was sponsored by Jiga, we do honestly believe that the rapid manufacturing industry needs to change and that Jiga has a chance to improve real problems with sourcing.